Mortgage rates in the United States have dropped to their lowest level in more than three years, offering a welcome shift for homebuyers and homeowners watching borrowing costs closely. The latest data shows borrowing conditions improving just as the housing market approaches the busy spring buying season.

According to newly released figures from Freddie Mac, the benchmark 30-year fixed mortgage rate declined again this week, signaling that housing affordability may be slowly improving after a long stretch of elevated rates.

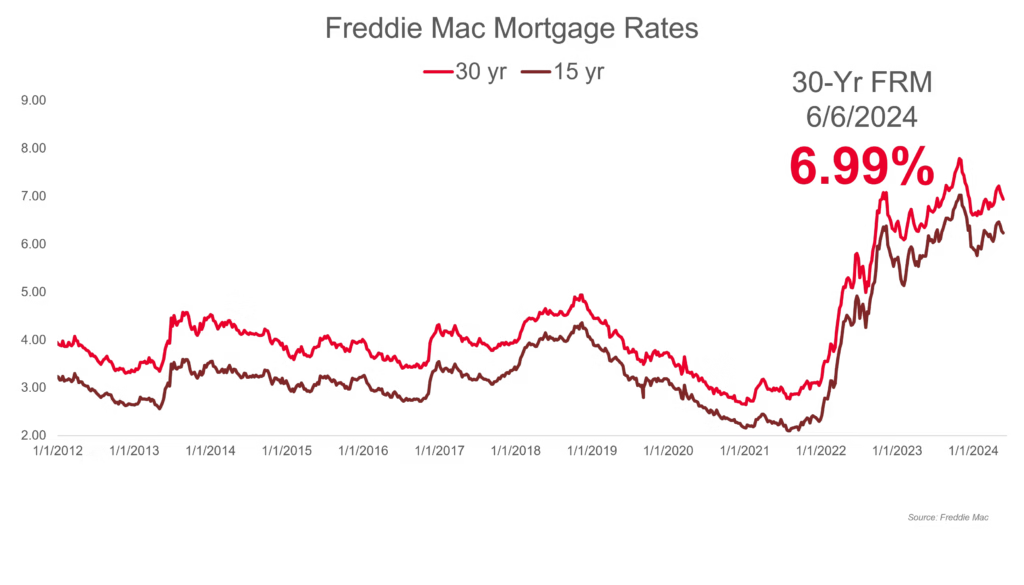

Mortgage Rates Drop To Multi-Year Low

Freddie Mac reported Thursday that the average rate for a 30-year fixed mortgage fell to 6.01%, down from 6.09% the previous week. That marks the lowest level since September 2022.

Just a year ago, the same mortgage averaged 6.85%, highlighting how dramatically borrowing costs have shifted over the past twelve months.

The decline could provide relief for buyers who had been waiting for lower financing costs before entering the housing market.

Lower Rates Help Buyers And Homeowners

Economists say the recent decline is already helping improve financial conditions for both prospective buyers and existing homeowners.

“This lower rate environment is not only improving affordability for prospective homebuyers, it’s also strengthening the financial position of homeowners,” said Sam Khater, Freddie Mac’s chief economist. “Over the past year, refinance application activity has more than doubled, enabling many recent buyers to reduce their annual mortgage payments by thousands of dollars.”

As refinancing activity rises, many homeowners are taking advantage of lower rates to cut monthly payments or adjust loan terms.

Shorter-Term Mortgage Rates Also Decline

Meanwhile, shorter-term mortgage rates moved lower as well. The average rate on a 15-year fixed mortgage dropped to 5.35%, down from 5.44% a week earlier.

Fifteen-year loans typically offer lower interest rates than longer-term mortgages, making them attractive to borrowers looking to pay off homes faster while saving on interest.

However, the shorter repayment period also means higher monthly payments compared with traditional 30-year loans.

Treasury Yields And Economic Data Influence Rates

Mortgage rates do not move independently. Instead, they closely track movements in the 10-year U.S. Treasury yield, which serves as a key benchmark for long-term borrowing costs.

As of Thursday afternoon, the 10-year Treasury yield hovered around 4.08%. Recent economic data has helped push that yield lower, contributing to the latest drop in mortgage rates.

“This dip from 6.09% last week follows a notable slide in the 10-year Treasury yield, which hit its lowest point since late November 2025 after last week’s softer-than-expected CPI reading and a relatively optimistic jobs report,” said Realtor.com senior economist Jake Krimmel.

Inflation trends, labor market conditions, and geopolitical developments all influence how investors price Treasury bonds, which in turn shapes mortgage rates.

Spring Homebuying Season May Get A Boost

The timing of the rate decline could play an important role as the housing market heads toward its busiest months of the year.

Lower borrowing costs typically increase purchasing power for buyers, making homes more affordable and expanding the range of properties they can consider.

Krimmel said the trend could continue if economic conditions remain supportive.

“There is a chance to be nearly a full percentage point lower than that this spring, which would meaningfully boost purchasing power,” he said. “However, the supply side remains mixed: new construction in 2025 finished behind 2024, and inventory growth has clearly lost steam.”

That means buyers may still face limited options even if financing becomes more favorable.

Housing Market Still Faces Supply Challenges

Despite the drop in mortgage rates, the broader housing market continues to struggle with limited inventory in many areas.

Construction activity slowed slightly in 2025 compared with the previous year, while the growth of available homes for sale has also cooled.

As a result, competition among buyers could remain strong if demand increases during the spring season.

Still, the latest mortgage data suggests that borrowing conditions are improving, potentially opening the door for more buyers who had been sidelined by high interest rates.

For now, economists and housing analysts will be watching closely to see whether falling rates translate into a more active housing market in the months ahead.